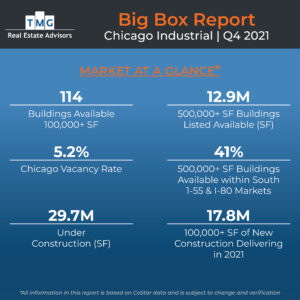

Big Box Report – Chicago Market Update

Industrial construction activity continues to hover near all-time highs in Chicago at approximately 31.0 million SF. Given the robust construction pipeline, deliveries are expected to continue at an elevated pace through at least 2022 and consistent with national trends, the vast majority of both under-construction and recently delivered space is in the logistics segment. Eight other Chicago area submarkets have at least 1 million SF of industrial space underway, as the significant rise in the demand for space has pushed development up across the Chicago region.

Chicago’s industrial market continues to see record levels of demand, as an astounding 36.2 million SF of space has been absorbed over the past year. This level of demand formation is more than 30% higher than the previous record high for Chicago of 24 million SF (set in 2004) and well over twice the average levels seen over the past five years. At the same time, leasing activity continued at a record clip in 2021, a signal that the strong pace of absorption will continue into 2022.

While demand for industrial space continues at a record clip, new supply continues to deliver at a robust pace, as approximately 17.8 million SF of new space has delivered over the past year. At the same time, approximately 31.0 million SF of industrial space is underway in Chicago. Over half of current under-construction space is being developed speculative, including four projects that exceed 1 million SF. With demand growth steadily outpacing new supply, vacancy within Chicago’s industrial market has declined by -1.5% over the past 12 months to its lowest point in over two decades at 5.0%.

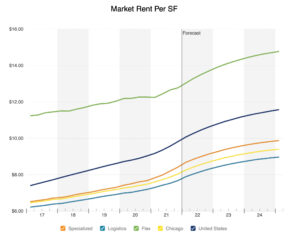

Buoyed by record levels of new demand and tight fundamentals, average industrial market rents continue to rise at a brisk pace in Chicago, most recently hitting a new all-time high of nearly $8.10/SF. Industrial rents have increased by an impressive 8.0% over the past year, slightly behind the national average of 9.0%. The specialized and logistics segments have seen the strongest rent growth in Chicago over the past year at 10.3% and 7.4%, respectively, while the flex segment has reported gains of 5.2% over the same time.

Demand formation in Chicago logistics segment has been even stronger than the market -wide totals at approximately 35.1 million SF over the past year. Thanks to this strong pace of demand formation, vacancy in the logistics segment has compressed by -2.1% over the past year to just 4.6%, its lowest level in over 15 years. The fundamental tightening seen in Chicago’s logistics sector has come despite the delivery of approximately 17.1 million SF of logistics space over the past year, the second most of any metro during that time.

The continued build-out of supply chains and brisk growth in ecommerce sales in response to the pandemic has pushed industrial leasing volume to new record highs in Chicago. Over 67.5 million square feet of space was signed for in 2021, a level that is nearly 40% higher than the average annual total leasing volume in the three years preceding the pandemic (2017-19) of approximately 48 million SF and well above the approximately 59 million SF of space signed for in 2020.

Rental growth has also continued at an above-average pace in the logistics segment over the past year at 7.4%. Looking forward, tight fundamentals and strong demand should continue to push industrial rents higher in Chicago, with CoStar’s baseline forecast currently calling for average industrial rents to grow by nearly 13% between now and the end of 2023.

Learn more at www.tmg-rea.com or contact us info@tmg-rea.com